Spatiotemporal and Network Volatility Models

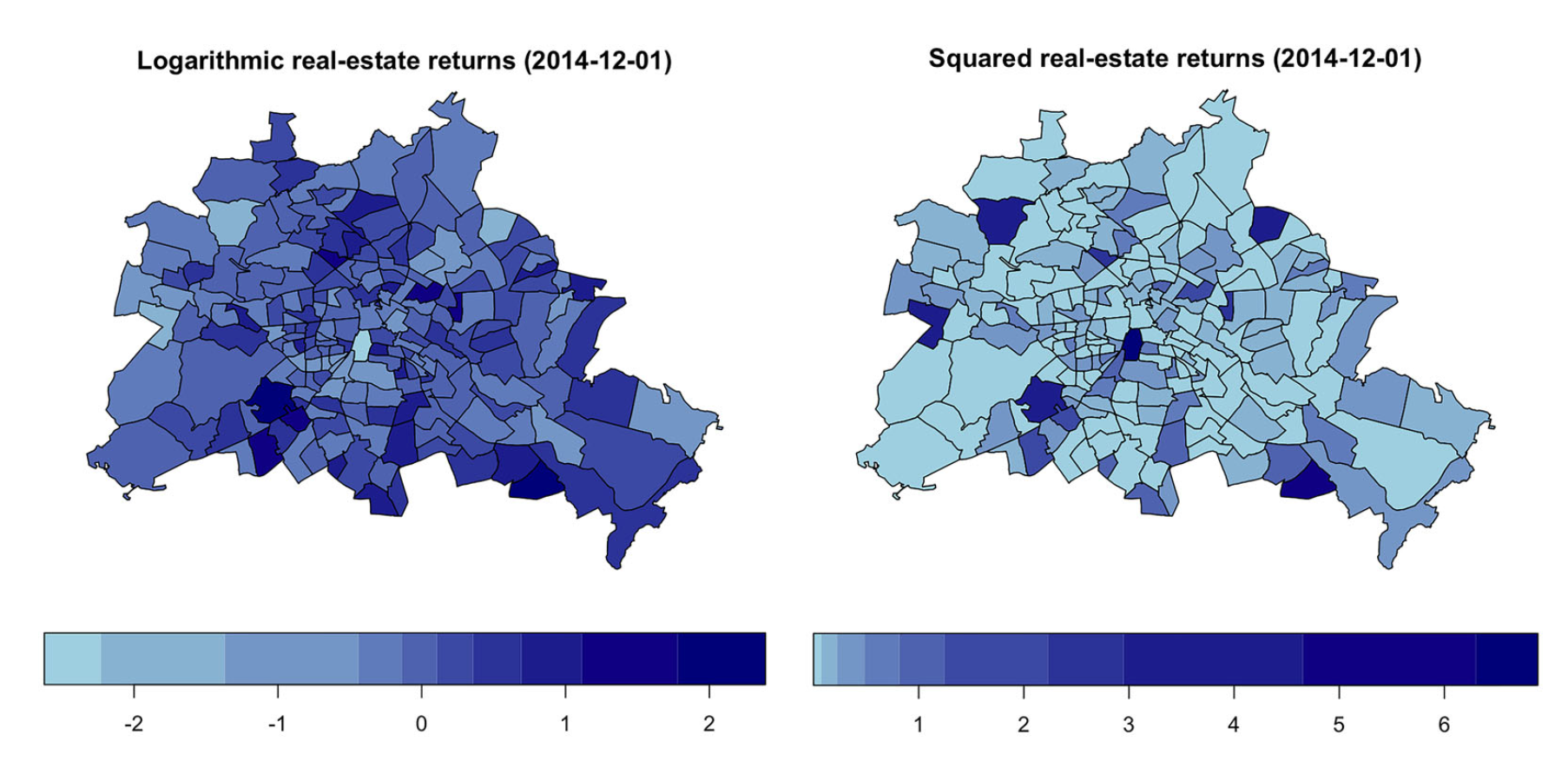

Researchers in the school are developing novel approaches to capture the complex dynamics of volatility across space, time, and networks. This work extends traditional financial econometric models by incorporating spatial and network dependence structures, enabling the modelling of volatility spillovers across regions or financial institutions. Recent research includes spatiotemporal GARCH-type models, network log-ARCH processes, and Markov-switching spatial volatility frameworks. Applications range from regional housing markets and stock return series to risk propagation in financial systems, with an emphasis on interpretable model structures and computational scalability for high-dimensional data.

Researchers

Publications

- Otto, P., Dogan, O., Taspinar, S., Schmid, W., Bera, A. K. (2025): Spatial and Spatiotemporal Volatility Models: A Review. Journal of Economic Surveys. → Authoritative overview and conceptual synthesis of spatial and network volatility models.

- Otto, P. (2024): A multivariate spatial and spatiotemporal ARCH model. Spatial Statistics. → General framework for multivariate volatility modelling over space and time.

- Mattera, R., Otto, P. (2024): Network log-ARCH models for forecasting stock market volatility. International Journal of Forecasting. → Novel network-based volatility model for financial risk forecasting.

- Otto, P., Dogan, O., Taspinar, S. (2024): Dynamic Spatiotemporal ARCH Models. Spatial Economic Analysis. → Extension of ARCH models incorporating spatiotemporal autoregression.

- Otto, P., Fülle, M. (2023): Spatial GARCH Models for Unknown Spatial Locations – An Application to Financial Stock Returns. Spatial Economic Analysis. → Addresses volatility modelling with partially unknown spatial structures."