2026 Election Policy Insights: The Global Economy and Scotland

Published: 5 May 2026

5 May 2026: Next up in our Election Policy Insights series, Professor Sir Anton Muscatelli examines Scotland's economic outlook amid growing global instability, writing that the pressures sharpen the case for renewed focus on Scotland's economic growth.

5 May 2026: Next up in our Election Policy Insights series, Professor Sir Anton Muscatelli examines Scotland's economic outlook amid growing global instability, writing that the pressures sharpen the case for renewed focus on Scotland's economic growth.

Policy Insights by Professor Sir Anton Muscatelli

Hard Choices Ahead: Scotland’s Policy Outlook in a More Fragile Global Economy

Setting the context: Scotland’s fiscal starting point

The current Holyrood election campaign underlines a growing disconnect between the political debate and the scale of the economic challenges Scotland now faces. The party manifestos and the campaign have focused on commitments to public services and living standards. Yet the fiscal and economic context in which the next Scottish Government will operate is becoming markedly more difficult, shaped both by domestic pressures and by renewed instability in the global economy.

The starting point is Scotland’s medium term fiscal outlook. The most recent Scottish Government Medium Term Financial Strategy – drawing upon forecasts from the Scottish Fiscal Commission (SFC) – has estimated that, by 2029–30, the incoming Scottish Government will face a fiscal gap of around £4.8 billion. This assessment has been echoed by a range of independent analysts, including the Institute for Fiscal Studies and the Fraser of Allander Institute. Despite this broad consensus, the implications of this gap have received limited attention in the election campaign.

As the SFC has pointed out, the pre-election budget made some assumptions as part of forward plans which will be hard if not impossible to deliver. These include very substantial efficiency savings — around £1.5 billion over the next three years, with £1 billion assumed in health alone — alongside reductions in the public sector workforce and tight pay settlements that imply real terms cuts in public sector wages. In addition, one off revenues, notably Crown Estate income linked to offshore wind leasing, have been used to support ongoing expenditure. While such measures can provide short term relief, they do not resolve the underlying mismatch between spending commitments and sustainable revenues.

The global backdrop: the Iran War as an economic shock

These domestic pressures are now being amplified by developments in the global economy. Since 2020, a sequence of macroeconomic shocks has already weakened economic resilience across advanced economies: the pandemic, supply chain disruption, and energy and commodity price volatility following Russia’s invasion of Ukraine. This has strained public sector finances across the advanced economies, including the UK. The Iran War represents a further and potentially more destabilising shock, particularly through its impact on energy markets and critical inputs to agriculture and manufacturing.

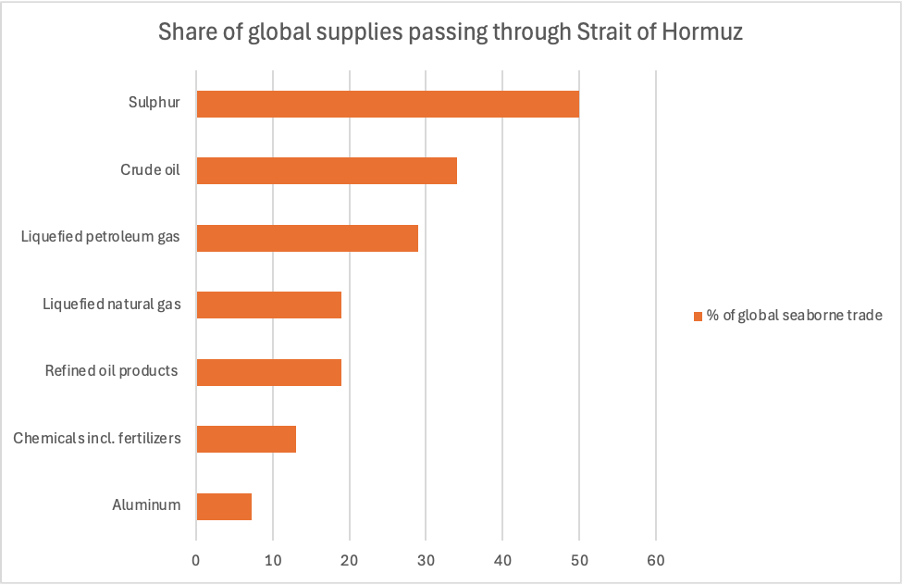

The global economy remains heavily exposed to disruption in the Strait of Hormuz. Critical oil and gas infrastructure has also been damaged in the Gulf region and will take months or years to repair and restore full production. Around 34% of global oil and oil product exports flow through the Strait of Hormuz, and almost 20% of global liquefied natural gas (LNG) trade and 29% of liquefied petroleum gas (LPG).

Beyond oil and gas, the region plays a significant role in the supply of petrochemicals, fertilisers, helium and aluminium, all of which are essential inputs in sectors ranging from food production to semiconductors and medical equipment. Many food producing countries are heavily impacted by the impact on fertilizer prices. Prolonged disruption therefore risks feeding into both higher inflation and weaker growth. This is a classic stagflation shock which will hit the world economy in 2026-27. The chart below, drawn using World Bank data shows the significance of the Strait for seaborne trade of some key commodities.

Source: World Bank Commodity Markets Outlook, April 2026

What the evidence says: growth, inflation and fiscal risk

Recent forecast updates from international institutions highlight these risks. The OECD and IMF have recently updated their global economic forecasts. While the IMF’s central projection assumes a relatively contained shock, the UK has seen one of the largest downward revisions to growth among G7 economies in its April forecast compared to January. GDP growth is now expected to be 0.8% in 2026 instead of 1.3%, and 1.3% in 2027 instead of 1.5%. The OECD similarly has reduced their previous forecast for UK GDP growth for 2026 by 0.5% in their March interim report.

But the IMF’s central scenario is actually quite benign in terms of what it assumes about the resolution of the Iran War. It assumes that oil and gas prices will experience a 20% increase (with oil averaging $82 per barrel) compared to 2025 before returning to the baseline in mid-2027. The G7 fiscal and monetary policy response is also expected to be muted. The OECD forecast just takes forward prices for commodities, which in March were still relatively subdued.

Things could, realistically get much, much worse, if the crisis does not abate quickly: and there is little sign of an early resolution. The IMF highlights two further downside scenarios with more adverse assumptions — involving sustained increases in energy and commodity prices alongside tighter financial conditions. These would see global growth slowing sharply to 2% in 2026 in the worse-case scenario, and global inflation in 2026 and 2027 between 5.5-6%. For the UK a shock of this magnitude might imply stagnation or even a recession. With such an uptick in inflation feeding through to the UK economy, the Bank of England would have no alternative but to act if this was seen to increase UK inflation expectations.

For fiscal policy, these scenarios matter greatly. Since the 2025 Budget, interest rates on UK government debt (so-called gilt yields) have risen by 60 basis points (at the time of writing). Gilts are the debt which the UK Government issues to borrow, and at around 5%, UK government is having to pay much more in interest rates to service its debt than it did a few years ago. In 2025-26 the UK’s independent fiscal watchdog, the Office for Budget Responsibility (OBR) expects UK government debt interest to total £111.2 billion, which is 8.3% of total public spending. Higher inflation and interest rates directly worsen the public finance arithmetic. The OBR also estimates that a one percentage point rise in gilt yields would worsen the UK’s fiscal balance by around £16 billion by the end of the decade.

This will feed through to pressures on Scotland’s fiscal position. With an increase in inflation, the outgoing Scottish Government’s assumptions about public pay would seem even less realistic. There would be pressures to increase spending on specific Scottish welfare payments that don’t have an equivalent block grant adjustment as these would be reduced in real terms, and public service spending would also be eroded in real terms.

There are also important structural pressures on the horizon. The UK Government has committed to raising defence spending from around 2.3 per cent of GDP today towards 2.5 per cent by 2027, with ambitions to go further in the longer term. While parts of the Scottish economy may benefit from higher defence expenditure, Scotland’s budget could come under further pressure through the operation of the Barnett formula, if there is a switch from devolved to reserved spending.

Are the political parties in Scotland thinking about the biggest fiscal challenge since devolution?

One of the reasons that Scottish political parties have been reluctant to speak about the looming fiscal gap, is that they may implicitly assume that additional UK funding will become available later in the parliament, as the Chancellor is forced to “re visit” (i.e. increase) existing spending review plans as we approach a UK election. That assumption now looks increasingly uncertain. Even a relatively mild global downturn would make it much harder for the UK government to relax fiscal constraints. The expectation that a future UK “fiscal cavalry” will come over the horizon in 2027-30 to resolve Scotland’s funding challenge risks might prove ill founded.

Taken together, these factors point to a sobering conclusion. The next Scottish Government is likely to inherit the most challenging fiscal position since devolution. Deferred choices will become unavoidable. This will require difficult decisions on public sector reform, the sustainability of welfare spending, and potentially higher taxation. However, tax increases are problematic, not only because Scotland has already opened up income tax differentials with the rest of the UK which may disincentivise economic growth, but also because realistically increasing Scottish income taxes further will not generate sufficient income to offset a fiscal gap of several billions. The main hope for a future Scottish Government would be that the UK Government might increase spending funded by higher UK taxes.

During this Scottish election campaign, we have heard some of the political parties trail what might be done to offset the impact of the Iran War on the cost of living. Putting aside whether some of the proposals (e.g. price controls on supermarket food) are legal under the UK Internal Market Act, it seems unlikely that short-term measures such as price controls on food and rents are workable as they will simply cause shortages. Any short-term support through the welfare system needs to be highly targeted on low-income households. My advice to our new Scottish Government and Parliament would be to focus less on the immediate short-run impact of the stagflation shock, and more on the long-run consequences of the shock which will impact on the livelihoods of Scottish households. Indeed, we should learn some lessons from how much the UK Government’s untargeted energy price support cost the exchequer in 2022-23.

Conclusion: Public trust, realism and long-term growth

Indeed, these global economic pressures sharpen the case for a renewed focus on Scotland’s economic growth. Improving growth will ultimately drive living standards and offset the initial shock. Scotland’s weaker relative tax growth continues to erode the resources available through the fiscal framework. Yet growth — in productivity, labour force participation and the tax base — rarely features centrally in our political debates. Without a coherent strategy to strengthen economic performance and resilience, fiscal pressures will intensify rather than ease.

The Royal Society of Edinburgh prepared a pre-election report stressing the need for a new approach to policy development: focusing on the long-run, and involving the public in what will be challenging debates on future policy choices. It was interesting that the public events around Scotland which the RSE undertook to engage citizens with the issues which matter to voters brought out the public’s desire for more honest engagement. Public trust in politics is declining, and our new Parliament and Government need to address this urgently.

From a public policy perspective, the priority now should be greater realism. The challenges facing Scotland are not unique, but they are acute. A more honest debate about fiscal trade-offs, alongside a clearer focus on long term growth, is essential if policy is to move beyond short term fixes and confront structural constraints more directly.

Author

Professor Sir Anton Muscatelli is Distinguished Honorary Professor at the University of Glasgow, a Senior Fellow of the Centre for Public Policy, and President of the Royal Society of Edinburgh.

Download and read this CPP 2026 Election Policy Insights: The Global Economy and Scotland as a PDF

Election 2026 Policy Insights

The Centre for Public Policy’s Election Policy Insights series seeks to enhance and inform the key debates defining the future of the country, offering comprehensive insight on policy issues and ways forward.

Image by Suzy Hazelwood from Pexels via Canva Pro

First published: 5 May 2026

Author

Professor Sir Anton Muscatelli is Distinguished Honorary Professor at the University of Glasgow, a Senior Fellow of the Centre for Public Policy, and President of the Royal Society of Edinburgh.

Election 2026 Policy Insights

The Centre for Public Policy’s Election Policy Insights series seeks to enhance and inform the key debates defining the future of the country, offering comprehensive insight on policy issues and ways forward.

CPP on Elections 2026

Visit our dedicated elections webpage for more expert insights.

Download and read this CPP 2026 Election Policy Insights: The Global Economy and Scotland as a PDF