How Macroprudential Policies Shape Corporate Investment: Firm-Bank Level Evidence from European Countries

Published: 13 May 2025

Research insight

A new study by Koray Alper (European Investment Bank), Soner Baskaya and Shuren Shi (both University of Glasgow) finds that tighter macroprudential policies reduce business investment in physical assets, especially for smaller firms, while R&D remains largely unaffected.

Background

Following the Global Financial Crisis (GFC), policies to enhance financial stability have become increasingly prevalent, including the formalization of macroprudential policies (MaPs) frameworks designed to mitigate systemic risks and prevent future crises. However, less attention has been given to an important question: how do MaPs affect real businesses, particularly firms’ investment decisions?

Using detailed firm-bank-level data from 27 European countries, our new study, “How do macroprudential policies affect corporate investment? Insights from EIBIS data”, sheds light on this issue. We find that when MaPs are tightened, corporate investment falls — but not uniformly. Investments in physical assets like machinery and infrastructure drop noticeably, while investment in intangible assets, such as R&D and employee training, remains largely unaffected.

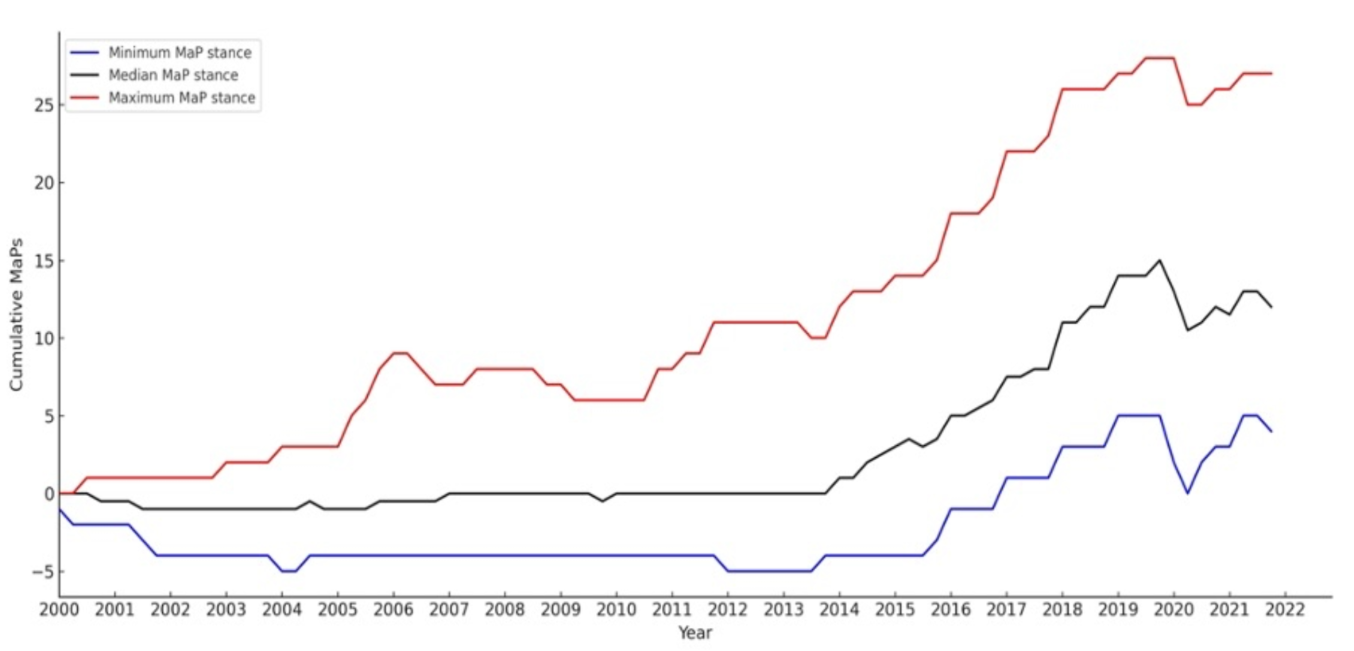

This figure illustrates the evolution of the macroprudential (MaP) policy stance from 2008 to 2022, displaying the minimum, median, and maximum values across the countries in our sample. We sum the dummy-type indicators (1 for tightening actions, 0 for no change, and -1 for loosening actions) for policy action indices covering 17 macroprudential tools at the country level across time. Since the GFC, the EU 27 have deployed MaPs more actively, with tightening actions significantly outnumbering loosening measures

Figure 1. Macroprudential Policy Stance

Why do macroprudential policies matter for firms?

Corporate investment — buying equipment, building facilities, expanding operations — is critical for economic growth. Yet firms often rely heavily on bank financing for these investments. Macroprudential policies influence banks' willingness and ability to lend, which in turn shapes firms' access to credit. When lending conditions tighten, businesses may have to scale back investment plans.

Our study shows that following MaP tightening, firms report higher loan rejection rates and lower satisfaction with loan terms, especially regarding the amounts they are offered. Companies increasingly rely on internal financing rather than external loans. This evidence suggests that MaPs primarily affect corporate investment through the bank lending channel.

Which firms are most affected?

The impact of MaPs is not uniform across all firms. Smaller businesses, financially weaker firms, and those linked to less resilient banks are hit hardest. Investment by micro firms and large corporations is much less affected, likely because larger firms have better access to alternative financing, while micro firms are less dependent on external loans to begin with.

Understanding these differences is important. If MaPs unintentionally constrain investment mainly among SMEs — the backbone of many economies — this could have lasting effects on productivity and growth.

Does the type of macroprudential measure matter?

Not all MaPs have the same impact. Our analysis finds that supply-side measures — such as higher capital requirements for banks — have a stronger negative effect on corporate investment than demand-side measures that target borrowers, such as limits on loan-to-value or debt-to-income ratios.

This distinction matters for policymakers. Designing macroprudential policies that safeguard financial stability without unnecessarily restricting business investment requires understanding these different transmission channels.

What about different types of investment?

One of the more encouraging findings is that intangible investment — such as R&D and employee training — appears largely unaffected by MaP tightening. This contrasts with tangible investment — physical assets like equipment and buildings — which declines significantly.

The reason lies in financing patterns. Firms often fund intangible investments with internal resources, partly because intangible assets are harder to pledge as collateral. In contrast, tangible investments depend more heavily on bank financing, making them more sensitive to changes in credit supply.

Given the growing importance of intangible assets in modern economies, it is reassuring that macroprudential tightening does not appear to hinder innovation-related investment.

Policy implications

Our findings suggest that while macroprudential policies play a vital role in maintaining financial stability, they are not without side effects. Tighter regulations can reduce corporate investment, particularly among smaller and financially constrained firms.

This does not mean MaPs are a mistake — far from it. Stronger banks and a safer financial system benefit the economy over the long term. However, policymakers should be mindful of the short-term trade-offs. Calibrating MaPs carefully and considering complementary support measures for SMEs during periods of regulatory tightening, could help mitigate unintended consequences.

A deeper understanding of these dynamics will be important as governments continue refining their macroprudential frameworks.

Read the full report on the European Investment Bank website.

First published: 13 May 2025